Shopping has changed over the past half century. The range of buyers has changed since the relative stability of the 1970s and earlier, which was fairly consistent in the post-World War II era.

Shopping has changed over the past half century. The range of buyers has changed since the relative stability of the 1970s and earlier, which was fairly consistent in the post-World War II era.

Retail shopping is moving from the mall-centric, personal experiences of the 1960s to the omnichannel approach of 2024. Modern shoppers combine online and in-store interactions, leveraging technology for convenience, personalization and sustainability. The development of artificial intelligence, e-commerce and data analysis now promotes customer engagement, in contrast to the earlier simpler, more product-focused, personal shopping.

A recent development includes sustainability and ethical consumption as a major trend, with some consumers favoring environmentally friendly and socially responsible brands.

However, most major studies show that the best valueis still king, especially in the post-pandemic era of inflation and political instability in the United States.

In this article, we examine both of these new realities and present a case study that assesses how consumers feel about sustainability and social responsibility in relation to retail corporate behavior. These consumers are divided into three categories based on a simple Q-factor segmentation.

Next, we introduce a technique called the Value Index. In this approach, respondents rate 15 retailers on a perceived value scale of 1 to 5. The value index then ranks these detections and we present an efficient way to display the results.

Finally, how do our three consumer groups perceive value among our group of companies? A visual perceptual map or correspondence analysis illustrates this by showing which of the top 15 general merchandise retailers in the United States most closely align with each consumer group.

A Brief History of Retail Wars

When I was growing up in the 1970s, Sears, Kmart, and Woolworths were giant retailers that had commanded everyone’s attention for the foreseeable past. By the 1980s, Walmart, Target, and JC Penney had become strong competitors, challenging Sears and Kmart in the U.S. retail market.

In 1990, Walmart became the nation’s largest general merchandise retailer by annual sales, overtaking Kmart and Sears. The fear that Walmart would destroy the United States began to gain significant traction in the 1990s and early 2000s. This period marked Walmart’s rapid expansion across the country and its rise to become the largest retailer in the United States and the world. In addition, Costco introduced its membership warehouse club model in the 1990s, offering bulk merchandise at competitive prices and high-quality private label products.

In the 2000s, the Internet changed all. That year saw the start of Amazon’s dominance and the consolidation of industries into large corporations such as Home Depot (home goods), Best Buy (electronics), and Michaels (arts and crafts). CVS Health has grown significantly, acquired Aetna, and expanded its role in healthcare beyond traditional pharmacy services.

The 2000s marked a seismic paradigm shift in consumer behavior. Since 2000, retail shopping has undergone a dramatic transformation due to advances in technology, changes in consumer behavior and the changing retail environment. The rise of e-commerce, mobile shopping, multi-channel retailing, the ubiquity of smartphones and personalization have all shaped the era of Amazon and online shopping.

So, who’s on top now?

Factor Analysis – A Snapshot of Consumer Attitudes

In this case study, the first step in cluster analysis is called the “Q-factor”. This involves conducting a factor analysis of the questions and attitudes within each of the four attitude clusters in the example. In our case, we asked respondents to rate on a scale of 1 to 5 whether they agree with the statements (see below).

Figure 1 – Factor analysis of corporate behavior statements

Factor analysis uses a regression technique to create variables for each factor. Each respondent receives a factor loading (similar to a correlation coefficient) for each factor. The respondent is placed in the factor with the highest load.

Figure 2 – Segmentation frequency table of the factor analysis

A quick note: Although this article is a pseudo-case study, the percentages in the table above are roughly consistent with my studies over the past year. While a significant number of consumers are concerned about corporate behavior or environmental policies, value remains the primary driver.

Value measurement comparison

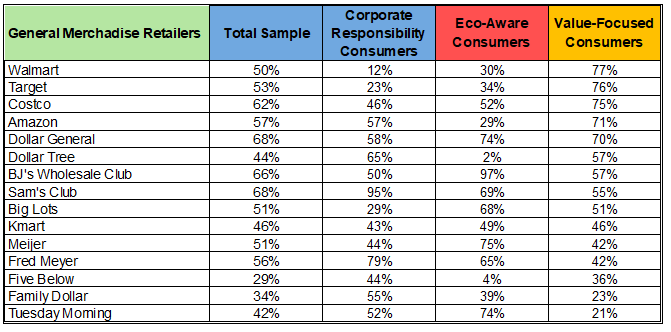

Respondents were then shown a list of the best general merchandise stores and asked to rate their value on a scale of 1 to 5. Below are the top 2 box (4 of 5) percentages overall and by our three consumer groups.

Figure 3 – The Top 15 General Merchandise Retailers in the United States, Ranked by Annual Revenue

If we index the average Top 2 Box scores and use them, we get a table that ranks the perceived value of each general merchandise retailer.

Figure 4 – Top 15 General Merchandise Retailers in the United States by Indexed Value

Correspondence analysis – Perceptual maps

Perceptual mapping is a graphical technique used by marketers that attempts to visually represent the perceptions of customers or prospects. Generally, the position of a product, product line, brand or company is shown in relation to competitors. Proximity of brand attributes indicates brand association with the rest of the map.

Proximity, not quadrant, is the actionable insight for perceptual maps. I like to explain to clients that brands, or in our case consumer groups (red labels) are planets and stores (blue labels) are moons. The closer a red label is to a blue one, the more consumers in that group identify with their nearest moon against all other consumer groups and retailers.

I like Perceptual Maps along with the Value Index for the following reasons. Correspondence maps offer a more concise and visual way to analyze data than straight percentage tables. They allow you to simultaneously examine the relationships between rows and columns in a contingency table, revealing patterns, associations, and trends that might not be immediately apparent in raw percentages. Correspondence maps provide a snapshot of the entire stew, making it easier to identify similarities or differences between our different customer types and retailers’ associated value perceptions during analysis.

Figure 5 – Perception map The most popular general merchandise retailers

Examining the map, we see that three companies attach value to corporate responsibility. Dollar General stands between Corporate Responsibility and Eco-Awareness. Within the Eco-Aware segment, four retailers associate environmental friendliness as a value more than others. Additionally, four of the “big” large general merchandise retailers are more closely associated with corporate positions related to value rather than responsibility or environmental friendliness.

Conclusion

In summary, the display of value for top general merchandise retailers provides crucial insight into how these companies position themselves on key attributes such as corporate responsibility and eco-awareness. Perceptual maps can be used to identify distinct clusters of retailers that prioritize different aspects of value, enabling a more nuanced understanding of market positioning.

This visual presentation highlights not only the competitive situation, but also the varied value propositions offered to consumers. Understanding these dynamics enables better strategic decision-making, helping retailers align their brand strategy with consumer expectations and market trends. Ultimately, this analysis underscores the importance of value perception in shaping consumer decisions and driving business success.

Michael Lieberman is the founder and president of Multivariate Solutions, a statistics and marketing research consultancy that works with major advertising, public relations and political strategy firms. He can be reached at 1.646.257.3794 or at michael@mvsolution.com.