The global mining and steel industry A transformer enters decades, led by decarbonization requirements, automation technologies and geopolitical reorganization. According to BIS Research, the industry is estimated at $ 875.7 billion in 2024 and is expected to reach $ 1.45 trillion by 2035, registering 4.63%. From digital twin mines to hydrogen furnaces, the future of metals and minerals becomes smarter, clearer and more strategic.

The global mining and steel industry A transformer enters decades, led by decarbonization requirements, automation technologies and geopolitical reorganization. According to BIS Research, the industry is estimated at $ 875.7 billion in 2024 and is expected to reach $ 1.45 trillion by 2035, registering 4.63%. From digital twin mines to hydrogen furnaces, the future of metals and minerals becomes smarter, clearer and more strategic.

Infrastructure Megings: Steel’s Demand Supercher

The steel industry growth focuses on ruthless global demand for infrastructure. Countries such as India are aimed at triple steel capacity – reaching 500 million tonnes by 2047, by states such as Odisha and Chhattisgarh, which are rich in ore. The Indian government quickly monitors mining auctions, simplified land purchase and introduced national steel policy to develop raw materials.

At a global level, the Chinese Belt and Road Initiative and the US Bipartial Infrastructure Act promote the need for flat and long steel products used in roads, bridges and electrical network developments. With 70% of the steel used in infrastructure and construction, these mega -cycles will fix demand well over the next decade.

Electrical Production: Rise in EAF and Green Hydrogen

Traditional domes are enhanced by electric arc furnaces (EAFS) and direct reduced iron (DRI) processes. EAFS allows for waste steel, while DRI processes are now connected to green hydrogen instead of carbon-based.

An example of this: H2 green steel In Sweden, one of the world’s first large -scale green steel plants is being built, driven completely renewed hydrogen. The project targets 5 million tonnes a year with almost zero emissions. Similarly, Steel He announced a plan of £ 2 billion to convert Scunthorpe’s plant to EAFS by 2027, reducing carbon intensity by more than 75% (Times, May 2025).

In Australia, in 2025, $ 636 million was launched to create a new hydrogen steel facility in Whyalla, allowing the country to compete globally in low-carbon steel exposure (Reuters, February 2025).

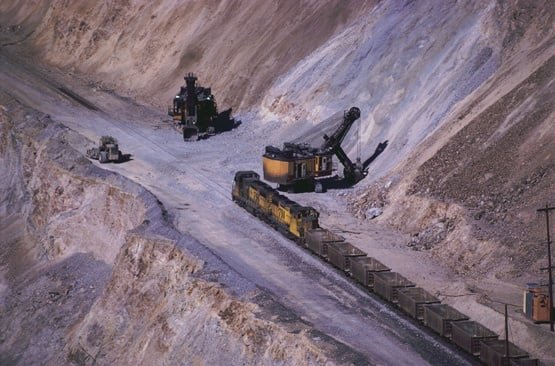

Digitization in Mining: AI, IoT and Autonomous Shipment

On the mining side, the fourth industrial revolution is in progress. Companies install real-time GIS analysis, AI-based ore classification and autonomous trucks to enhance efficiency and security.

The Gudai-Darri mine in Rio Tinto in Australia is a flagship smart mine, which is carried out by digital twin technology, 5G connection and autonomous drilling tower. These innovations reduced the time period by 30% and increased the ore refund by 15%, according to the company’s 2025 ESG performance report.

AI -TA is also used for predictive maintenance, allowing companies to detect equipment failures before they happen. Coupled with the Internet (IoT) sensors embedded in conveyors and crushes, this data -oriented approach converts traditional extraction operations into smart, adaptable systems.

Circular steel and waste renaissance

The steel industry now sees waste not as waste, but as a strategic resource. Electric arc furnaces (EAFS) that rely on waste, not the virgin iron ore, lead this charge. In particular, Europe witnesses that waste trade regulations are increasing, as countries are trying to keep the materials domestically to produce green steel.

The recent article published on ARXIV (2024) emphasizes that the EU should measure waste collection and selection infrastructure by 3x to achieve climate-neutral steel purposes. Policy decision -makers are considering a “waste passport” system to monitor origin and quality, helping to avoid carbon leaks through imported dirty waste.

Strategic sources and geopolitics

Nickel, cobalt and rare earth – are essential for green steel and EV batteries – are at the heart of the geopolitical competition. Indonesia has become the main player and takes advantage of Nikkel’s reserves to attract more than $ 20 billion in Chinese investment posts for the 2014 RAW ORE export ban. The Bahodop Industrial Park is today one of the largest nickel -spinning junctions in the world (Ft, May 2025).

Meanwhile, the United States’ inflation reduction law and the EU’s critical raw material law encourage domestic procurement and refinement of strategic minerals, leading to the reorganization of global supply chains.

The previous road: smarter, greener, more flexible

As mining and steel industry The convergence of re -configurations, automation, decarbonization and strategic resource planning determines its path. Investments in AI-driven research, hydrogen-based metallurgy and closed loop material systems not only improve operational indicators, but also redefine competitiveness in the carbon-limited world.

In order to flourish in the new era, industry leaders need to adjust capital costs to accept green technology, deepen the transparency of ESG and localize supply chains. Tomorrow’s metals will not only be stronger – smarter and more sustainable.

About the publisher: BIS Research is a global market intelligence, research and consulting company that focuses on emerging technological trends that are likely to interfere with the market. In his team, industrial veterans, experts and analysts have various backgrounds in the field of consulting, investment banking, government and academy.